Can we use ointment which contains lanolin (wool fat) from sheep?

Answer:

In the Name of Allah, the Most Gracious, the Most Merciful.

As-salāmu ‘alaykum wa-raḥmatullāhi wa-barakātuh

It is permissible to use ointments and creams that contain lanolin extracted from sheep’s wool.

Discussion

Lanolin is a natural fat obtained from sheep’s wool, not from the flesh, blood, or fat of the animal in the sense of consumption. Wool, hair and similar by-products are considered pure even if the animal was not slaughtered.[1]

وأما شعر الميتة وعظمها وصوفها وقرنها فلا بأس بالانتفاع بها وبيع ذلك كله جائز وأما العصب ففيه روايتان في رواية جاز الانتفاع به وبيعه كذا في المحيط (الفتاوى الهندية 3/115 دار الفكر)

A 55-year-old male, currently in the state of Ihram for Umrah, uses a CPAP machine for obstructive sleep apnea during sleep. The CPAP mask covers approximately one-fourth of his face and is worn for 6-8 hours at night. What is the ruling of ihram?

Answer:

In the Name of Allah, the Most Gracious, the Most Merciful.

As-salāmu ‘alaykum wa-raḥmatullāhi wa-barakātuh.

Since the CPAP mask covers a substantial portion of the face and is worn for six to eight hours at night, he will be required to either offer a minor expiation (ṣadaqah) or fast for one day.

Discussion

Normally, if one covers one quarter of the face or more for the duration of a full day or a full night (12 hours) continuously, then a major expiation (damm) becomes obligatory; if the duration is less than that, then a minor expiation (ṣadaqah) is required.[1] This excludes anything that is not normally used to cover the face (e.g. wood).[2]

However, because it was done out of need, if a person wears it for longer than twelve hours, which would normally necessitate a major penalty (damm), he will have the choice of doing three things:

Fasting 3 days, or

Feeding six poor persons, giving each the equivalent of ṣadaqat al-fiṭr, or

Offering a sacrifice (damm) within the boundaries of the Haram.

If it is worn for less than twelve hours, which would normally necessitate a minor penalty (ṣadaqah), then he will have the choice between:

Based on this principle, since a CPAP mask covers approximately one quarter of the face and is worn only for six to eight hours at night, which does not amount to a full night (twelve hours), and as it is worn out of necessity, he will have the choice between offering a minor expiation (ṣadaqah) or fasting for one day.

And Allah Ta’āla Knows Best

Answered by

Habib Ullah Khan

Checked & Approved By

(Mufti) Muadh Chati

[1] آج کل جراثیم سے بچنے کے فیشن میں بحالتِ احرام چہرے پر ’’ماسک‘‘ لگانا عام ہوگیا ہے، تو اس بارے میں شرعی حکم اچھی طرح یاد رکھنے کی ضرورت ہے کہ احرام میں اس طرح ’’ماسک‘‘ پہننا مردوں اورعورتوں سب کے لئے بلاشبہ ممنوع ہے، اور جزاء کے بارے میں تفصیل یہ ہے کہ اگر ’’ماسک‘‘ اتنا چوڑا ہے کہ اس سے چوتھائی چہرہ ڈھک جاتا ہے اور یہ ’’ماسک‘‘ مسلسل بارہ گھنٹے لگائے رکھا تو دم واجب ہے، اور اگر ’’ماسک‘‘ کی چوڑائی چوتھائی چہرے سے کم ہو یا اسے ۱۲؍گھنٹے سے کم لگایا تو صدقۂ فطر واجب ہوگا؛ اس لئے بہرحال احرام کی حالت میں ’’ماسک‘‘ نہیں لگانا چاہئے۔

کتاب النوازل :٧ /٣٧٥ ط. مکتبہ جاوید دیوبند

صورت مسئولہ میں ماسک چونکہ چہرے کے جوتہائی یا زیادہ حصہ کو چھپا لیتا ہے لہذا اگر ایک مکمل دن یا ایک مکمل رات یا زیادہ پہنا ہے تو دم واجب ہوگا اور اس سے کم استعمال کیا ہے تو صدقہ لازم ہوگا

فتاوی دار العلوم زکریا: 3/453 ط. زمزم پبلشرز

وإن غطى المحرم ربع رأسه أو وجهه يوما فعليه دم، وإن كان أقل من ذلك فعليه صدقة، وأما المحرمة فإنها تغطي كل شيء منها إلا وجهها، فإن غطته يوما فعليها دم… إن كان المحرم نائما فغطى رجل رأسه ووجهه بثوب يوما كاملا فعليه دم، ألا ترى أنه لو انقلب في نومه على صيد فقتله كان عليه جزاؤه

المختصر الكافي: 1/308 ط. مكتبة الأمام الذهبي للنشر والتوزيع

(ولنا) حديث «الأعرابي حين وقصت به ناقته في أخافيق جرزان، وهو محرم فقال – صلى الله عليه وسلم – لا تخمروا رأسه ووجهه»، وفي هذا تنصيص على أن المحرم لا يغطي رأسه ووجهه «، ورخص رسول الله – صلى الله عليه وسلم – لعثمان – رضي الله عنه – حين اشتكت عينه في حال الإحرام أن يغطي وجهه» فتخصيصه حالة الضرورة بالرخصة دليل على أن المحرم منهي عن تغطية الوجه، ولأن المرأة لا تغطي وجهها بالإجماع مع أنها عورة مستورة فإن في كشف الوجه منها خوف الفتنة فلأن لا يغطي الرجل وجهه لأجل الإحرام أولى، وتأويل الحديث بيان الفرق بين الرجل والمرأة في تغطية الرأس.

المبسوط للسرخسي: 4/ 9 ط. دار الكتب العلمية

(قال): وإن غطى المحرم ربع رأسه أو وجهه يوما فعليه دم، وإن كان دون ذلك فعليه صدقة وعن أبي يوسف – رحمه الله تعالى – قال: إن غطى أكثر رأسه فعليه دم وإلا فعليه صدقة؛ لأن القليل من تغطية الرأس لا تتم به الجناية والقلة والكثرة إنما تظهر بالمقابلة، وهذا أصل أبي يوسف – رحمه الله تعالى – في المسائل، وفي ظاهر الرواية الجواب قال: ما يتعلق بالرأس من الجناية فللربع فيه حكم الكمال كالحلق، وهذا لأن تغطية بعض الرأس استمتاع مقصود يفعله الأتراك وغيرهم عادة بمنزلة حلق بعض الرأس فأما المحرمة تغطي كل شيء منها إلا وجهها وتلبس كل شيء من المخيط وغيره إلا الثوب المصبوغ فإن فيما لا حاجة بها إلى لبسه فهي بمنزلة الرجل وفيما تحتاج إلى لبسه وستره يخالف حالها حال الرجل، وقد بيناه

المبسوط للسرخسي: 4/ 140-141 ط. دار الكتب العلمية

أما المرأة فعليها أن تغطي رأسها ولكن لا تغطي وجهها ثم في الجواب ظاهر الرواية إذا غطى ربع الرأس أو الوجه يوما واحدا يجب عليه الدم وإن كان أقل من يوم يجب عليه الصدقة بقدره

تحفة الفقهاء: 1/420 ط. دار الكتب العلمية

وبتغطية نصف وجهه أو رأسه ما يجب بكله.

خزانة الأكمل: 1/364 ط. دار الكتب العلمية

المُحرم لو اتزر بالسَّراويل أو توشح بالقميص لا بأس به. لو أدخل منكبيه في القباء ولم يُدخِلْ يديه في الكمين جاز. لو غطّى رأسَه يوماً أو حَضَبَ فعليه دم، وإن كان أقل فصدَقة.

(الفتاوي السراجية: 186-187 ط. دار الكتب العلمية

وكذا لو غطى ربع رأسه يوما فصاعدا فعليه دم، وإن كان أقل من الربع فعليه صدقة، كذا ذكر في الأصل. وذكر ابن سماعة في نوادره عن محمد أنه لا دم عليه حتى يغطي الأكثر من رأسه، ولا أقول: حتى يغطي رأسه كله. وجه رواية ابن سماعة عن محمد: أن تغطية الأقل ليس بارتفاق كامل، فلا يجب به جزاء كامل. وجه رواية الأصل أن ربع الرأس له حكم الكل في هذا الباب، كحلق ربع الرأس وعلى هذا إذا غطت المرأة ربع وجهها وكذا لو غطى الرجل ربع وجهه عندنا وعند الشافعي لا شيء عليه؛ لأنه غير ممنوع عن ذلك عنده، والمسألة قد تقدمت ولو عصب على رأسه، أو وجهه يوما أو أكثر فلا شيء عليه؛ لأنه لم يوجد ارتفاق كامل وعليه صدقة؛ لأنه ممنوع عن التغطية.

بدائع الصنائع: 3/212 ط. دار الكتب العلمية

ولا يغطى المحرم رأسه ولا وجهه والمحرمة لا تغطى وجهها، وإن فعلت ذلك إن كان يوماً إلى الليل فعليها دم، وإن كان أقل من ذلك فعليها صدقة، وكذلك إذا غطى ربع رأسه فصاعدا يوماً، فعليه دم، وإن كان أقل من ذلك، فعليه صدقة، هكذا ذكر في المشهور. وعن محمد رحمه الله تعالى أنه قال: لا يجب الدم حتى يغطى الأكثر من الرأس، والصحيح ما ذكر في المشهور؛ لأن ما يتعلق بالرأس من الجناية، فللربع مثل الكل. المحيط البرهاني: 3/430 ط. إدارة القرآن

إذ ليس فساد الصلاة بانكشاف الربع لذلك بل لعده كثيرا عرفا، وليس الموجب هذا هنا؛ ألا ترى أن أبا حنيفة لم يقل بإقامة الأكثر مقام الكل في اليوم أو الليل الواقع فيهما التغطية واللبس؛ لأن النظر هنا ليس إلا لثبوت الارتفاق كاملا وعدمه، وكذا إذا غطى ربع وجهه أو غطت المرأة ربع وجهها.

قوله (يوما كاملا أو ليلة) الظاهر أن المراد مقدار أحدهما، فلو لبس من نصف النهار إلى نصف الليل من غير انفصال أو بالعكس لزمه دم، كما يشير إليه قوله: وفي الأقل صدقة، شرح اللباب،

رد المحتار: ٢/٥٤٧ ط. ایچ ایم سعید

[2] محرم اگر اپنے سر یا چہرہ کو کسی ایسی چیز سے ڈہانکے جس سے عموما سر ڈہانکنے کا کام نہیں لیا جاتا یے مثلا چہتری، لکڑی، لوہا، پیتل اور شیشہ وغیرہ، تو اس میں کوئی حرج نہیں ہے

کتاب المسائل: 3/179 ط. المرکز العلمی للنشر والتحقیق

[3] ما ذكرنا من لزوم الدم عينًا أو الصدقة عينًا في فصل الطيب واللبس، ومنه التغطية والحلق وقلم الأظفار إنما هو في حالة الاختيار بأن ارتكب المحظور بغير عذر، أما في حالة الاضطرار بأن ارتكبه بعذر كمرض وعلة، فإن كان مما يُوجب الدم فهو مخيَّر بين الصيام والصدقة والدم ولو موسرا، ولو أدى الثلاثة عن كفارة واحدة لا يقع إلا واحد وهو ما كان أعلى قيمة، ولو ترك الكل يُعاقب على ترك واحدٍ منها، وهو ما كان أدنى قيمةً؛ لأن الفرضَ يَسقُط بالأدنى ( كبير ). وإن كان مما يُوجب الصدقة فهو مخيَّر بين الصيام والصدقة، قال في «رد المحتار»: «وليست الأربعة قيدا، فإنّ جميع محظورات الإحرام إذا كان بعذر ففيه الخيارات الثلاثة اهـ»، ونقل مثله في (الكبير)…..

وإذا وجب الدم مخيرا إن شاء ذَبح في الحرم أو تصدق بثلاثة أصوع طعام، أو ستة من غيره على ستة مساكين أين شاء (در )، لكل مسكين نصف صاع من بر أو صاعا من غيره حتى لو تصدّق بها على ثلاثة لم يجز إلا عن ثلاثة؛ وعليه تكميل الباقي، ولو تصدق بها على سبعة على السوية لم يجز أصلا؛ لأن العدد منصوص عليه، وسيأتي تمامه (بحر)، أو صام ثلاثة أيام إن شاء ولو متفرقة. وإن وجب الصدقة على التخيير إن شاء تصدّق بما وجب عليه من نصف صاع أو أقل على مسكين أو صام يوما (رد المحتار) عن «اللباب».

غنية الناسك في بغية المناسك: ص 406/ص 408 ط. المصباح

فإن لبس المحرم ما لا يحل له من الثياب أو الخفاف يوماً أو أكثر من ذلك لضرورة، فعليه أي الكفارات شاء وقد بينا فيما سبق أن ما يجب الدم بلبسه في غير موضع الضرورة إذا لبسه لأجل الضرورة يتخير فيه بين الكفارات ما شاء

المبسوط: 4/141 ط. دار الكتب العلمية

إذا فعل ذلك بعلة أو ضرورة فعليه أي الكفارات شاء، كذا في( الشرح الطحاوي) وذلك إما النسك، أو الصدقة، أو الصوم، فإن اختار النسك ذبح في الحرم، كذا في (المحيط) وإن ذبح في غير الحرم لا يجوز عن الذبح، إلا إذا تصدق بلحمه على ستة مساكين، على كل واحد منهم قيمة نصف صاع من الحنطة، كذا في (الشرح الطحاوي). وإن اختار الصوم، صام ثلاثة أيام في أي مكان شاء، كذا في (المحيط) إن شاء تابع، وإن شاء فرق، كذا في (شرح الطحاوي). وإن اختار الصدقة، تصدق بثلاثة أصوع حنطة على ستة مساكين، لكل مسكين نصف صاع والأفضل أن يتصدق على فقراء مكة، ولو تصدق على غير فقراء مكة جاز، كذا في (المحيط)، ويجوز فيه التمليك وطعام الاباحة على قول أبي حنيفة وأبي يوسف رحمهما الله تعالى، وعند محمد رحمة الله تعالى : لا يجوز فيه إلا التمليك كذا في (البدائع) و(الظهيرية) و(الشرح الطحاوي (.

الفتاوى الهندية: 1/308 ط. دار الفكر

[3] وأما بيان ما يجب بفعل هذا المحظور ؛ وهو لبس المخيط : فالواجب به يختلف في بعض المواضع : يجب الدم عيناً، وفي بعضها : تجب الصدقة عيناً، وفي بعضها: يجب أحد الأشياء الثلاثة غير عين، الصيام، أو الصدقة، أو الدم، وجهات التعيين إلى من عليه، كما في كفارة اليمين، والأصل: أن الارتفاق الكامل باللبس يوجب فداء كاملاً، فيتعين فيه الدم – لا يجوز غيره إن فعله من غير عذر، وإن فعله لعذر فعليه أحد الأشياء الثلاثة، والارتفاق القاصر يوجب فداء قاصراً؛ وهو الصدقة إثباتاً للحكم على قدر العلة. وبيان هذه الجملة : إذا لبس المخيط من قميص أو جبة أو سراويل، أو عمامة أو قلنسوة، أو خفين أو جوربين، من غير عذر وضرورة يوماً كاملاً – فعليه الدم، لا يجوز غيره؛ لأن لبس أحد هذه الأشياء يوماً كاملاً ارتفاق كامل ؛ فيوجب كفارة كاملة وهي الدم، لا يجوز غيره؛ لأنه فعله من غير ضرورة. وإن لبس أقل من يوم لا دم عليه، وعليه الصدقة.

بدائع الصنائع: 3/211 ط. دار الكتب العلمية

اگر بیماری وغیرہ کے عذر سے سلا ہوا کپڑا پہنا، یا خوشبو استعمال کی یا بال کٹوائے یا سر کو یا چہرے کو کپڑے سے چھپایا، یا عورت نے چہرے کو کپڑے سے اس طرح چھپایا کہ کپڑ اس کے چہرے کو لگا ہوا رہا، تو ان سب صورتوں میں اگر جنایت کامل ہوئی، تو اختیار ہے کہ دم دے یا تین روزے رکھے یا چھ مسکینوں کو بقدر صدقۃ الفطر صدقہ دے، یعنی ہر مسکین کو پونے دو کلو گندم یا اس کی قیمت دے اور اگر جنایت کامل نہیں تو دو چیزوں کا اختیار ہے کہ جو صدقہ واجب ہوا ہے، یعنی ایک صدقۃ الفطر مقدار کی وہ ادا کرے یا اس کے بدلے ایک روزہ رکھے (ارشاد الساری) ایک صدقہ دے یا ایک روزہ رکھے تین یا دو چیزوں میں اختیار صرف عذر کی حالت میں ہے-

A person is having trouble whilst washing their face during Wudu, due to the eczema, what should they do in this case? Jazakallah

Answer:

In the Name of Allah, the Most Gracious, the Most Merciful.

As-salāmu ‘alaykum wa-raḥmatullāhi wa-barakātuh.

If an individual is unable to wash a limb required for wuḍūʾ due to harm or injury or that wetness may delay healing (based on personal experience or the advice of a doctor), then they should act according to what is possible, and their wuḍūʾ will remain valid. This is done as follows:

If washing the limb is harmful, they should wipe over the limb, provided wiping does not cause harm.

If wiping the injured limb itself is also harmful, then they should wipe (masaḥ) over the bandage or dressing covering that limb, as wiping over a dressing is permitted when direct contact would cause harm.

If wiping (masah) over the bandage is likewise harmful or not possible, the limb is excused and omitted, and the wuḍūʾ remains valid.[1]

If the majority of the body parts that are required to be washed in wuḍūʾ are such that wetness may cause harm or delay healing, such that they cannot be washed, then it is permitted to perform tayammum.[2] In such a case, one will not resort to wiping (masah) of the body parts, instead one will do tayammum.

And Allah Ta’āla Knows Best

Answered by

Habib Ullah Khan

Checked & Approved By:

(Mufti) Muadh Chati

[1] (ويجمع) مسح جبيرة رجل (معه) أي مع غسل الأخرى لا مسح خفها بل خفيه. (ويجوز) أي يصح مسحها (ولو شدت بلا وضوء) وغسل دفعا للحرج (ويترك) المسح كالغسل (إن ضر وإلا لا) يترك (وهو) أي مسحها (مشروط بالعجز عن مسح) نفس الموضع (فإن قدر عليه فلا مسح) عليها. والحاصل لزوم غسل المحل ولو بماء حار، فإن ضر مسحه، فإن ضر مسحها، فإن ضر سقط أصلا. (در المختار)

(قوله لا مسح خفها إلخ) أي لا يجمع مسح جبيرة رجل مع مسح خف الأخرى الصحيحة؛ لأن مسح الجبيرة حيث كان كالغسل يلزم منه الجمع بين الغسل والمسح، بل لا بد من تخفيف الجريحة أيضا ليمسح على الخفين، لكن لو لم يقدر على مسح الجبيرة له المسح على خف الصحيحة صرح به في التتارخانية: أي؛ لأنه كذاهب إحدى الرجلين (قوله بلا وضوء وغسل) بضم الغين بقرينة الوضوء، وهذا هو الثالث، ولا يتكرر على قوله الآتي، والمحدث والجنب إلخ؛ لأن هذا فيما إذا شدها على الحدث أو الجنابة، وذاك فيما إذا أحدث أو أجنب بعد شدها أفاده ح (قوله ويترك المسح كالغسل) أي يترك المسح على الجبيرة كما يترك الغسل لما تحتها، وهذا هو الرابع ح (قوله إن ضر) المراد الضرر المعتبر لا مطلقه؛ لأن العمل لا يخلو عن أدنى ضرر وذلك لا يبيح الترك ط عن شرح المجمع (قوله وإلا لا يترك) أي على الصحيح المفتى به كما مر (قوله وهو إلخ) هذا الخامس (قوله عن مسح نفس الموضع) أي وعن غسله، وإنما تركه؛ لأن العجز عن المسح يستلزم العجز عن الغسل ح (قوله ولو بماء حار) نص عليه في شرح الجامع لقاضي خان، واقتصر عليه في البدائع، وقيده بالقدرة عليه. وفي السراج أنه لا يجب والظاهر الأول بحر

حاشية ابن عابدين: 2/234-236 ط. دار السلام

قوله: (وَإِلا لا يُتْرَكُ) قال في البحر) عن المحيط» إذا زادت الجبيرة على رأس الجرح إن كان حل الخرقة وغسل ما تحتها يضر بالجراحة يمسح على الكل تبعًا، وإن كان الحل والمسح لا يضران بالجرح لا يجز به مسح الخرقة، بل يغسل ما حول الجراحة، ويمسح عليها لأعلى الخرقة، وإن كان يضره المسح، ولا يضره الحل يمسح على الخرقة التي على رأس الجرح، ويغسل حواليها، وتحت الخرقة الزائدة إذ الثابت بالضرورة يتقدر بقدرها، ولو ضره الحل لا المسح يمسح كما صرح به في «الدرر». قوله: (وهو مشروط … إلخ) هو الخامس قوله: (عن مسح نفس الموضع) والعجز على المسح يستلزم العجز عن الغسل حلبي قوله: (فإن قدر عليه) أي: على مسح نفس الموضع، وعجز عن غسله قوله: (فلا مسح عليها) أي: صحيح. قوله: (ولو بماء حار) في الشرنبلالية عن قاضي خان» إن كان لا يضره غسل ما تحتها يلزمه الغسل، وإن كان يضره الغسل بالماء البارد لا بالحار يلزمه الغسل بالماء الحار؛ أي إن قدر عليه قاله الكمال. قال الشارح: قوله: (فإن ضر) أي: غسله، ولو بماء حار مسحه افتراضا، فإن ضر مسحه مسح الجبيرة افتراضا قوله: على كل عصابة) الصواب أن يقال: على كل العصابة؛ لأن كلا إذا دخلت على منكر، أفادت استغراق الأفراد، وإذا دخلت على معرف أفادت استغراق الأجزاء والمقصود الثاني، ثم إن المصنف تبع الكنز) في ذلك، والأصح الذي عليه الفتوى الاكتفاء بمسح الأكثر. قال في «البحر»: وكان ينبغي للمصنف أن يقول: ويمسح على أكثر العصابة ونحوها، وإن لم يكن تحتها جراحة إن ضره الحل، انتهى، وهل الدواء كالجبيرة في هذا الحكم؟ يحرر، أفاده الحلبي.

حاشية الطحطاوي على الدر المختار: 1/144 ط. مكتبه رشيديه

“وإن كان أكثره صحيحا غسله” أي الصحيح “ومسح” الجريح” بمروره على الجسد وإن لم يستطع فعلى خرقة وإن ضره تركه وإذا كان الجراحة قليلة ببطنه أو ظهره ويضره الماء صار كغال الجراحة حكما للضرورة “ولا” يصح أن “يجمع بين الغسل والتيمم” إذ لا نظير له في الشرع للجمع بين البدل والمبدل والجمع بين التيمم وسؤر الحمار لإداء الفرض بأحدهما لا بهما كما لا يجتمع قطع وضمان وحد مهر ووصية وميراث إلى غير ذلك من المعدودات هنا.

مراقي الفلاح شرح نور الإيضاح: 52 ط. دار الكتب العلمية

ولو كان أكثر بدنه صحيحا وأقله جريحا ثم أجنب أو أحدث غسل الصحيح ومسح الجريح إن لم يضره، وعلى الخرقة إن ضره وتيمم لو كان عكسه

فتح باب العناية بشرح النقاية: 1/103 ط. دار الكتب العلمية

[2] 569 – وإذا كان عامة بدن الجنب جريحًا، أو عامة أعضاء المحدث، فإنه يتيمم ولا يستعمل الماء فيما كان صحيحاً. وإن كان على العكس، فإنه يغسل ويمسح على الجراحة إن أمكنه، أو فوق الخرقة إن كان المسح يضره، ولا يتيمم، وهو قول علماءنا رحمهم الله تعالى.

المحيط البرهاني: 1/314 ط. المجلس العلمي

إذا كان عامة بدن الجنب أو عامة أعضاء المحدث جريحاً يتيمم. وعلى عكسه يغسل الصحيح. ويمسح الجريح أو الخرقة إن لم يضره المسح.

المجتبى شرح مختصر القدوري: 1/86 ط. دار الرياحين

وإذا كان عامة بدن الجنب جريحا وشيء منه صحيحا، أو عامة أعضاء المحدث جريحا وشيء منه صحيحا، فإنه يتيمم ولا يستعمل الماء فيما كان صحيحا، وإذا كان على العكس فإنه يغسل ماكان صحيحا ويمسح على الجراحة إن أمكنه أو فوق الخرقة إن كان المسح يضره ولا يتيمم، وهو قول علمائنا،

الفتاوي التاتارخانية: 1/380 ط. مكتبة فاروقية

(ولا يجمع بين الوضوء والتيمم) لما فيه من الجمع بين الأصل والخلف بخلاف الجمع بين التيمم وسؤر الحمار؛ لأن الغرض يتأدى بأحدهما لا بهما فجمعنا بينهما لمكان الشك (فإن كان أكثر الأعضاء) أي أكثر أعضاء الوضوء (جريحا) في الحدث الأصغر أو أكثر جميع بدنه في الحدث الأكبر (يتيمم) ولا يجوز أن يغسل الصحيح ويمسح الجريح. (وإلا) أي وإن لم يكن أكثر الأعضاء جريحا بل مساويا أو أكثر الأعضاء صحيحا (غسل الصحيح ومسح على الجريح) إن لم يضره وإلا فعلى الخرقة، ولا يجوز التيمم؛ لأن للأكثر حكم الكل.

مجمع الأنهر في شرح ملتقى الأبحر: 1/67 ط. دار الكتب العلمية

فإن كان أكثر أعضاء الوضوء جريحاً تيمَّم ولم يستعمل الماء، وإن كان أكثر أعضائه صحيحاً، غسل الصحيح ويمسح الجراحة إن أمكنه مسحه من غير ضرر، حتى لو كانت الجراحة على رأسِه ووجهه ويدِه وليس على رجليه جراحة يُباح له التيمم، وعلى عكسه لا يباح، وقيل: يعتبر الكثرة في الأعضاء حتى لو كان على رأسه ووجهه ويديه جراحة وليس على رجليه جراحة لا يباح له التيمم إذا لم يكن الأكثر من كلّ عضو جريحاً.

فتاوي قاضي خان: 1/39 ط. دار الفكر

قوله: (وإلا تيمم) أي وإن لم يكن له ثمنه تيمم لتحقق العجز قال – رحمه الله – (ولو أكثره مجروحا تيمم) أي ولو كان أكثر أعضاء الوضوء منه مجروحا في الحدث الأصغر أو أكثر جميع بدنه مجروحا في الحدث الأكبر تيمم؛ لأن للأكثر حكم الكل قال – رحمه الله – (وبعكسه يغسل) أي إذا كان الصحيح أكثر من المجروح يغسل لما قلنا.

تبيين الحقائق: 1/136 ط. دار الكتب العلمية

– فلو كان جميع بدنه مجروحاً أو مقروحاً ويضره الماء، فإنه يتيمم، وفي حال الوضوء ينظر إلى عدد أعضاء الوضوء، حتى لو كان رأسه ووجهه ويداه مجروحة دون رجليه مثلاً، فإنه يتيمم، وفي العكس لا يجوز له التيمم، بل يغسل الصحيح ويمسح الجريح، وإذا كان المسح يضره يمسح فوق الضماد وفي الغسل ينظر إلى مساحة المجروح، فإذا كان أكثر البدن مجروحاً يتيمم، وبالعكس يغسل الصحيح ويمسح على الجريح كما تقدم. وهذا إذا كان يمكنه غسل الصحيح بدون إصابة الجريح، فلو كانت الجراحة بظهره مثلاً، وإذا صب الماء على رأسه سال عليها، يكون ما فوق الجراحة كحكمها. وإن كان الصحيح والجريح متساويين، فالأحوط غسل الصحيح ومسح الجريح. ويتيمم من كانت الجراحة في يديه، ولا يمكنه غسل وجهه وقدميه، ولا يجد من يوضئه.

الفقه الحنفي في ثوبه الجديد: 1/158-159 ط. دار القلم

If a person gave adhan in one masjid and read salah there, then went to a second masjid and gave adhan there for the same salah, it would be makrooh.

But what if he gave adhan in the first masjid and didn’t read salah there and instead also gave adhan in a second masjid? Some say this scenario is also makrooh, and others say this is permissible. Can you please clarify what the correct position is in this regard?

Answer:

In the Name of Allah, the Most Gracious, the Most Merciful.

As-salāmu ‘alaykum wa-raḥmatullāhi wa-barakātuh.

The underlying rule is that it is considered makrūh (disliked) for a person to give the adhān and leave the masjid without any valid reason.

If a person gives the adhān in one masjid and performs the ṣalāh there, thereafter he leaves to give the adhān in another masjid for the same ṣalāh, this is deemed makrūh.[i]

However, some jurists state that if the ṣalāh was not performed in the first masjid, and he goes to another masjid for a valid reason such as the congregational prayer not taking place without him, or because he is the mu’adhin there, or the only imam etc, then it is not disliked for him to leave[ii].

And Allah Ta’āla Knows Best

Answered by:

Shabbir Dewan

Checked & Approved By:

(Mufti) Muadh Chati

[i] ويكره أن يؤذن في مسجدين، ويصلي في أحدهما ؛ لأنه إذا صلى في المسجد الأول – يكون متنفلاً بالأذان في المسجد الثاني، والتنفّل بالأذان غير مشروع؛ ولأن الأذان يختص بالمكتوبات، وهو في المسجد الثاني يصلي النافلة، فلا ينبغي أن يدعو الناس إلى المكتوبة وهو لا يساعدهم فيها . بدائع الصنائع ١/٦٤٨ ط.دار الكتب العلمية وحاشية ابن عابدين ٢/٦٣٤ ط.دار السلام

ويكره أن يؤذن في مسجدين لأنه يكون في إحداهما داعيًا إلى ما لا يفعل. غنية المتملي ٢/٢٧٠ ط.الجامعة الاسلامية: دار العلوم ديوبند

قال : (ويكره أن يؤذن في مسجدين ويصلي في أحدهما) لأنه بعد ما صلى يكون متنفلاً بالأذان في المسجد الثاني والتنفل بالأذان غير مشروع ولأن الأذان مختص بالمكتوبات فإنما يؤذن ويقيم من يصلى المكتوبة على أثرهما، وهو في المسجد الثاني يصلى النافلة على أثرهما.كتاب المبسوط١/٢٨٦ ط.دار الكتب العلمية

[ii]) وكره خروجه من مسجد أذن فيه (أو في غيره )حتى يصلي (لقوله صلى الله عليه وسلم” :لا يخرج من المسجد بعد النداء إلا منافق أو رجل يخرج لحاجة يريد الركوع) “إلا إذا كان مقيم جماعة أخرى (كإمام ومؤذن لمسجد آخر لأنه تكميل معنى. مراقي الفلاح ٣٨٨

قوله : (وكره خروجه) أي تحريماً للنهي بالحديث المذكور… قوله : (كإمام) قيده في الكبير، وشرح السيد، وغيرهما بإمام تتفرق الناس بغيبته فيفيد أنه لو لم يكن بهذه المثابة لا يخرج، والظاهر أن المؤذن إذا كان من يقوم مقامه عند غيبته يكره له الخروج أيضاً. حاشية الطحطاوي على مراقي الفلاح ٤٥٧ ط.دار الكتب العلمية

اگر اس شخص پر دوسری مسجد کی جماعت کا توقف ہے کہ اگر یہ نہ جائے تو وہاں جماعت نہ ہو تب اس کو دوسری جگہ نماز پڑھنا مکروہ نہیں، وہیں جا کر نماز پڑھے، اگر اس پر توقف نہیں تو ایسی حالت میں مسجد سے نکلنا بلا ضرورت مکروہ ہے . فتاوی محمودیہ ٥/٤٣٧ط.ادارہ الفاروق کراچی

اگر دوسری مسجد میں جماعت کا انتظام اس سے متعلق ہے تو جانا جائز ہے، ورنہ مکروہ ہے ۔ آپ کے مسائل اور ان کا حل ٣/٣١٦ ط.مکتبہ لڈھیانوی

I have a query regarding the following, A friend of mine sells high value goods. To make it easy for customers, the customer has two options to pay for the goods:

1. Cash

2. Debit / Credit Card

3. EFT

If customer chooses to pay by debit / credit card, a 2% service fee is added to the invoice to cover the bank commission fee charged to seller. If customer chooses to pay by EFT, a higher price is charged by seller as seller is required to pay bank charges to withdraw the cash from the account again. Is this permissable from a shariah perspective? If this is not permissible, will it be permissible to quote the customer for the same goods a cash price and a different price form credit card or EFT?

Answer:

In the Name of Allah, the Most Gracious, the Most Merciful.

As-salāmu ‘alaykum wa-raḥmatullāhi wa-barakātuh.

Muhtaram Ulama,

The use of the credit card terminal is a norm. The seller is paid lesser than the value of the purchase price.

Where did the balance of the amount go?

Who took it?

Why?

Who are the role players between the seller and purchaser?

This complex issue has been thorougly researched by my able student, Moulana Maaz Chati which makes an interesting academic read.

May Allah Ta’ala increase Moulana Muadh in his Uloom. Ameen.

Ebrahim Desai

Hereunder are the details and procedures of a credit card transaction[1].

The individuals and institutions involved in a credit card transaction:

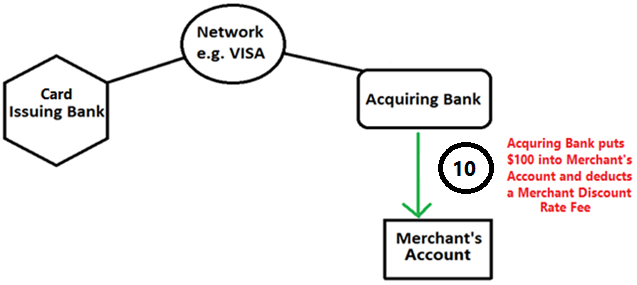

The Merchant: the individual selling the commodity.

The Customer: the individual buying the commodity.

The Card Issuing Bank: the Institution that has issued the card to the Customer and will pay for the commodity on behalf of the Customer.

The Acquiring Bank/Processor: the Institution that will acquire the payment for the commodity from the Card Issuing Bank on behalf of the Merchant.

The Merchant Account: this is the bank account of the Merchant. Once the Acquiring Bank/Processor gains posession of the payment from the Card Issuing Bank, the Acquiring Bank/Processor will deposit this payment into the Merchant’s account.

The Network: this is the organisation that liases between the Card Issuing Bank and Acquiring Bank/Processor.

EXAMPLE: VISA, MasterCard, American Express, Discover, etc.

The Fees

There are also 4 fees involved in the entire process[2]:

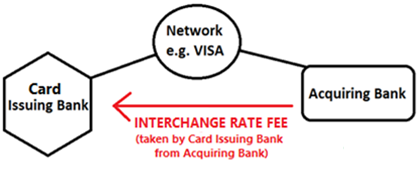

Interchange Fee: this is a fee taken by the Card Issuing Bank from the Acquiring Bank/Processor and remains constant for 6 months[3].

Network Fee: this is a fee taken by the Network (e.g. VISA) from the Acquiring Bank/Processor and remains constant.

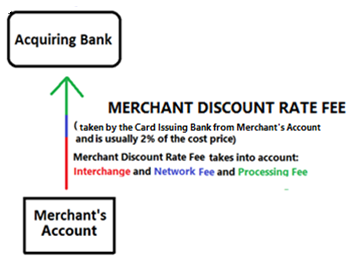

Merchant Discount Rate Fee: this is a fee charged by the Acquiring Bank/Processor to the Merchant and covers up for the Interchange Fee and Network Fee paid by the Acquiring Bank/Processor and includes a Processing Fee.

Processing Fee: It is a part of the Merchant Discount Rate Fee and is charged by the Acquiring Bank/Processor to the Merchant. This charge varies in Tiered Pricing and remains constant[4] in Interchage Plus Pricing.

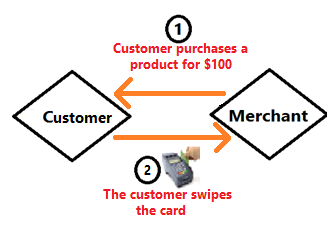

A transaction occurs between a Customer and a Merchant for a product that has a fee of $100,

The Customer swipes his credit card in the electronic terminal,

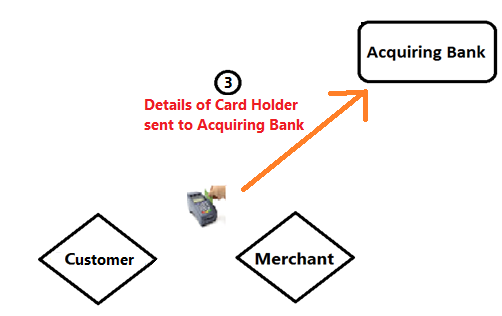

The Customer’s credit card details are sent to the Acquiring Bank/Processor,

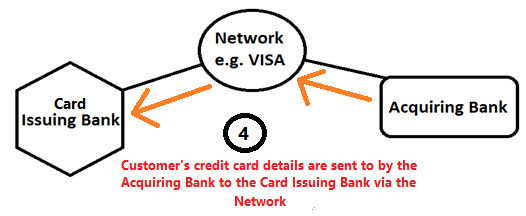

The Acquiring Bank/Processor sends the Customer’s credit card details to the Card Issuing Bank via the Network,

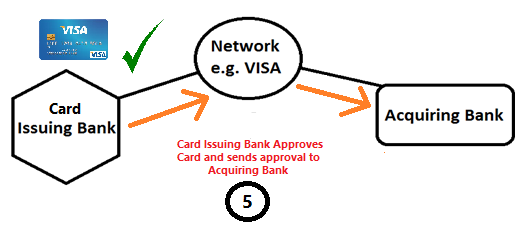

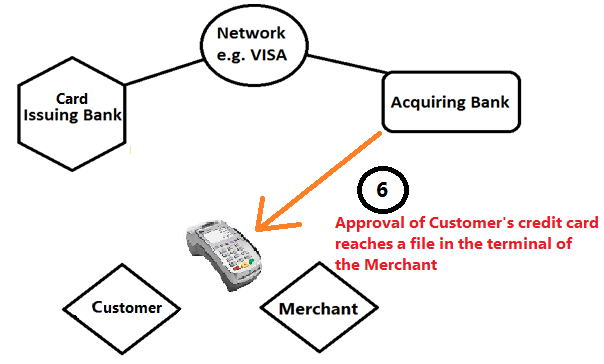

The Card Issuing Bank approves the Customer’s credit card and sends its approval to the Acquiring Bank/Processor,

The approval of the Customer’s credit card reaches the Merchant’s terminal and is stored in a file within the terminal,[6]

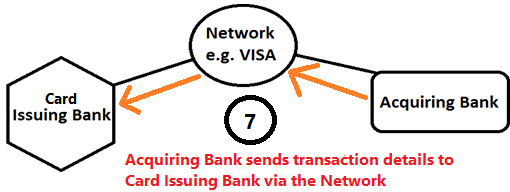

The Acquiring Bank/Processor sends the details of the transaction to the Card Issuing Bank through the Network,

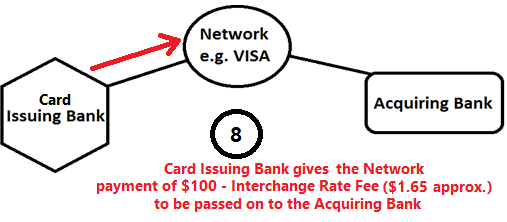

The Card Issuing Bank assesses the $100 payment and deducts approximately $1.65 as Interchange Fee, the remaining amount which is approximately $98.35 is then passed onto the Network and the Network will be required to pass on this amount to the Acquring Bank/Processor,

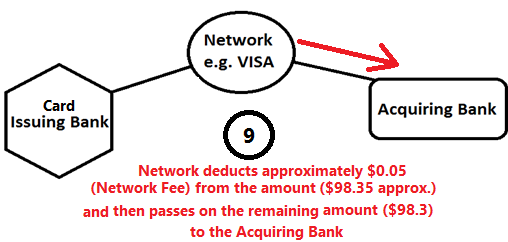

The Network deducts $0.05 (approx.) as a Network Fee from this remaining amount ($98.35 approx.), thus the Acquiring Bank/Processer receives approximately $98.3. The Acquiring Bank/Processor has lost $1.70 from the due payment of $100 due to the Interchange Fee and Network Fee,

The Merchant sends the terminal file to the the Acquiring Bank/Processor. The Acquiring Bank/Processor deposits $100 into the Merchant Account and deducts $2.00 (approx.) (approximately 2% of $100). This deduction of $2.00 (approx.) is a fee known as the Merchant Discount Rate Fee.[7]

Now, let us revisit the Fees that have been discussed:

There are 4 fees involved in the entire process[8]:

Interchange Fee: this is a fee charged by the Card Issuing Bank to the Acquiring Bank/Processor and remains constant for 6 months[9] (see point 8 above).

Network Fee: this is a fee charged by the Network (e.g. VISA) to the Acquiring Bank/Processor and remains constant (see point 9 above).

Merchant Discount Rate Fee (Approximately 2%): this is a fee charged by the Acquiring Bank/Processor to the Merchant and covers up for the Interchange Fee and Network Fee paid by the Acquiring Bank/Processor and includes a Processing Fee.

Processing Fee: It is a part of the Merchant Discount Rate and is charged by the Acquiring Bank/Processor to the Merchant[10] (see point 10 above).

A Summarised Version of the Above Procedure

Customer buys a product,

Customer swipes his credit card into the Merchant’s electronic terminal,

Details of the credit card are sent to the Acquiring Bank,

The Acquiring Bank sends the details of the credit card to the Card Issuing Bank through the Network,

The Card Issuing Bank approves the credit card,

The approval of the credit card is sent to the Merchant’s electronic terminal,

The Acquiring Bank now sends the details of the transaction to the Card Issuing Bank through the Network,

The Issuing Bank deducts a portion of the payment as Interchange Fee and delivers the balance to the Network,

The Network further deducts a portion from the balance as a Network Fee and delivers the remaining amount to the Acquiring Bank,

The Acquiring Bank transfers the payment to the Merchant’s account and deducts a percentage of the payment as a Merchant Discount Rate Fee.

The 2% Commission Fee (Merchant Discount Rate Fee)

It has been understood from the above that the 2% (approx.) charge paid by the Merchant to the Acquiring Bank/Processor is known as a Merchant Discount Rate Fee.

The Merchant Discount Rate Fee is made up of three components[11]:

Interchange[12][13][14] (the charge that the Acquiring Bank/Processor has paid to the Issuing Bank)

+ Network Fee[15] (the charge that the Acquiring Bank/Processor has paid to the Issuing Bank)

+ Processing Fee (added by the Acquiring Bank/Processor for its services)

Thus, the Merchant Discount Rate Fee is augmented due to the Interchange Fee[16] and Network Fee within.[17][18][19]

The reasons behind each charge

The Interchange Fee is charged by the Issuing Bank to the Acquiring Bank/Processor for the following reasons:

Bearing credit risk,

Fraud protection,

Benefits provided to the Merchant through the card.

The Network Fee is charged by the Network to the Acquiring Bank/Processor for the following reasons:

Providing a platform for the transaction,

Bearing risk, etc.

The Merchant Discount Rate Fee is charged by the Acquiring Bank/Processor to the Merchant for the following reasons[20]:

Acceptance of one or more payment brands,

Account services,

Terminal purchase or rental and ongoing maintenance, (this may be charged as a seperate invoice)[21]

Security upgrades,

Fraud risk management,

Interchange,

The use of data transmission lines,

Transaction slips and other card supplies,

Point-of-sale materials,

Acquirer’s profit margin.

The Shari’ah perspective

In principle, all costs incurred for the transfer of payment must be borne by the Customer[22] and all cost incurred for the delivery of the commodity must be borne by the Merchant.[23]

As mentioned above, the Merchant Discount Rate Fee is levied on the Merchant in lieu of various services provided to the Merchant.[24]Hence, it is not permissible for the Merchant to levy this charge onto the Customer.[25]

However, if it is the norm/common practise (urf – عرف) of the people of a region and sector[26] (such as some parts of the USA[27][28] and countries such as Australia[29]) to levy the Merchant Discount Rate Fee (2% approx.) upon the customer[30], then this would be permissible.[31]

However, the laws of the country wherein this is practised must be followed.[32]

Alternatively, the Merchant may increase the cost price of all products and then offer a discount to those who pay in cash in order to cover costs.[33]

Final Comments

It is important to understand that the concept of adding a service fee[34] to the invoice of the customer as proposed in the question has been considered illegal in some countries.[35][36] We must abide by the laws of the country in which we reside.[37]

As for increasing the cost price of products that are bought with a credit card/debit card/EFT at the time of sale as alluded towards in the question, this will be permissible[38] on the condition that the law of the country permits it.[39]

Alternatively, the Merchant may increase the cost price of all products[40] and then offer a discount to those who pay in cash; this is permissible[41] and is also legal.[42]

And Allah Ta’āla Knows Best

Answered by:

(Mufti) Muadh Chati

Checked & Approved By:

Mufti Ebrahim Desai.

[1]Debit cards and credit cards work in similar ways. Both carry the logo of a major credit card company, such as Visa or MasterCard, and can be swiped at retailers to purchase goods and services.

THE KEY DIFFERENCE BETWEEN THE TWO CARDS IS WHERE THE MONEY IS DRAWN FROM WHEN A PURCHASE IS MADE. WHEN A CONSUMER USES A DEBIT CARD, THE MONEY COMES DIRECTLY FROM HIS CHECKING ACCOUNT. WHEN HE USES A CREDIT CARD, THE PURCHASE IS CHARGED TO A LINE OF CREDIT FOR WHICH HE IS BILLED LATER.

Consider two customers who each purchase a television from a local electronics store at a price of $300. One uses a debit card, and the other uses a credit card. The debit card customer swipes his card, and his bank immediately places a $300 hold on his account, effectively earmarking that money for the television purchase and preventing him from spending it on something else. Over the next one to three days, the electronics store sends the transaction details to the bank, which electronically transfers the funds to the store.

The other customer uses a traditional credit card. When he swipes it, the credit card company automatically adds the purchase price to his outstanding balance. With most credit card companies, the customer has 30 days to pay before interest is charged on the outstanding balance. Interest rates on credit cards are notoriously high. Savvy consumers avoid paying credit card interest in two ways. One, they pay their balance in full each month and never allow it to carry over beyond the 30-day mark. Two, they use a debit card instead of a credit card and only spend money they have in their accounts.

Think of credit as borrowed money. This money is made available to you, but it must be repaid within an agreed amount of time. Credit cards provide a line of revolving credit. This differs from charge cards, which require that the balance is paid at the end of the month.

[2]Network Fees/Assessments are the fees charged by the Networks (MasterCard and Visa) to facilitate the transactions through their systems. They charge basis points of the transaction in the range of around 0.05% with fluctuations of several basis points in either direction.

Acquirer/Processor fees are charged by the merchant processor/acquirer and are highly variable. They are normally in the 10s of basis points (ie .10%-.70%) as a percentage of a transaction.

In a hypothetical example Chase is the card issuer, Visa is the network, First Data is the processor/acquirer. Transaction value of $100 with a merchant discount of 2%. The merchant only has to pay that 2% (they will pay that to their processor, First Data in this case). That processor passes this information to Visa who then allocates the $2.00 the following ways.

Interchange (assume 1.65%) –> $1.65 to Chase (set by Visa based off of the credit card used in the transaction)

Network Fee (assume 0.05%) –> $0.05 to Visa

Processor/Acquirer Fee (assume 0.30% –> $0.30 to First Data

This is very high level. More parties often charge additional fees such as gateways and additional types of merchant processors making the dynamics of a transaction layered with many companies each taking a sliver. Additionally the interchange levels set by the networks are complex documents with discounts, fees and assessments applied to various merchant classes, geographies and card types

Retailers and consumers do not pay interchange. Interchange is the transfer rate exchanged between the retailer’s and cardholder’s financial institutions each time a Visa payment product is used. The retailer’s financial institution, or acquirer, generally pays interchange. Retailers make a payment to their financial institution for Visa card transactions, frequently referred to as a Merchant Discount Rate (MDR). This is a market-based fee set by each acquiring financial institution operating in a competitive marketplace—retailers can choose their financial institution in the same way cardholders can choose the financial institution that issues their Visa card.

Interchange plus pricing means that the provider charges a set fee — say 0.10 percent + $0.05 — over the interchange rate (the fees that go to the bank that issued the card used to purchase the goods and services) and the pass-through fees (the fees charged by the card companies).

The advantage of interchange plus pricing is that you have a processing rate that is determined up front. If an interchange rate is adjusted up or down, it automatically takes effect and will only affect the rate on a few of the cards. With no hidden costs and a statement you can actually understand, you will be receiving the most competitive pricing available and it’ll be easier for you to compare to the other processors.

With true interchange plus pricing, the actual costs are passed through to the merchant and all the costs of the processing are disclosed for the merchant to see, including interchange and the dues and assessment costs, the processor will then work with the merchant to establish the discount rate.

There are two main kinds of pricing merchant service providers use, interchange plus and tiered.

Interchange Plus

An interchange plus pricing model, is basically just a markup model. The merchant service provider adds up the interchange and card brand fees for a transaction and then adds their standard markup rate on top of that. The markup rate does not change based on card provider or type, making it a pretty transparent pricing model.

A cardholder selects his or her goods, agrees to pay the retail price to the retailer and presents his or her card for payment.

The retailer submits the purchase details, including the Visa card information, to its acquiring financial institution for approval.

The acquiring financial institution sends the purchase details to the cardholder’s financial institution.

Assuming it has correctly followed the procedures required by its acquiring financial institution, the retailer receives a “payment guarantee,” and the cardholder receives the goods.

The cardholder’s financial institution remits to the retailer’s acquiring financial institution the retail price less the interchange rate. This interchange rate may be a unique rate that has been negotiated directly between the cardholder’s and retailer’s financial institutions, or it may be the default rate that is set by Visa.

Visa is not involved in any way with negotiating or setting the MDR.

(According to what is understood from Visa, the Interchange Fee is paid by the Acquiring Bank before the Merchant Discount Rate is taken from the Merchant. However, other websites show that the Interchage Fee is paid by the Acquiring Bank after the Merchant Discount Rate is taken from the Merhcant:

In the first step, the merchant sends its transactions to its merchant acquirer. The merchant acquirer sends this information to the merchant accounting system (MAS) servicing that particular merchant’s account. In some cases, the MAS is a part of the merchant acquirer; in others, it is a different entity. The MAS distributes the transactions to the appropriate network—Visa transactions to the Visa network, MasterCard transactions to the MasterCard network, and so forth.6 Next, the MAS deducts the appropriate merchant discount fee (to cover the costs of the merchant acquirer’s activities) from the transaction amount and generates instructions to remit the difference to the merchant’s bank for deposit into the merchant’s account. The MAS sends these instructions to the automated clearinghouse (ACH) network, which is a computer-based system used to process electronic transactions between participating depository institutions.

To recover these funds, the MAS sends information about the merchant’s transactions to Interchange, which is part of the Visa or MasterCard network. Interchange is the clearing and settlement sytem that transfers data between the card processor and the issuing bank. Interchange determines the interchange fee and Visa/MasterCard assessments (to cover the cost of the issuing bank’s services and the network’s costs) and sends the information to the card-issuing bank. In turn, the issuing bank remits the transaction amount, less the interchange fee, to Interchange, which passes it on to the MAS. Finally, the issuing bank bills the cardholder and collects the balance.

[6]So what really occurs when you make a purchase? Well, the credit card transaction often takes place within a minute, but it’s actually a complex process. When the credit card is swiped through an electronic terminal or sales unit, the credit card account’s information is read. The process of authorization can take place several ways but, generally, once it is read a request is sent for the authorization of the sale to the acquiring bank. The acquiring bank then sends the request to the cardholder’s issuing bank or card association, such as VISA. The issuing bank creates an approval or denial code. The code is sent back to acquiring bank and then to the electronic terminal. The merchant, typically, will pull out an additional receipt from the register when the process is complete. The receipt will either request your signature or deny your purchase based on the code that was transmitted. http://www.investopedia.com/university/credit-cards/credit-cards2.asp

[7]The retailer’s bank, or acquirer, remits to the merchant the retail price less the Merchant Discount Rate (MDR). Acquirers negotiate an MDR with a retailer for a package of electronic payment services and Visa is not involved in any way with negotiating or setting the MDR.

A merchant begins the settlement process by sending their batch of approved authorizations to their acquiring bank (or the bank’s processor). Authorization batches are typically sent at the close of each business day.

Acquirer

The acquiring bank (or its processor) reconciles and transmits the batch of authorizations through interchange via the appropriate card association’s network (VisaNet or Banknet).

The acquiring bank also deposits funds from sales into the merchant’s account via the automated clearinghouse (ACH) and debits its merchant’s account for processing fees either monthly, daily or both depending on the merchant’s processing agreement.

Card Network

The card association debits the issuing bank’s account and credits the acquiring bank’s account for the net amount of the authorizations which is gross receipts less interchange and network fees.

Issuer

The card issuing bank essentially pays the acquiring bank for its cardholder’s purchases.

Cardholder

The cardholder is responsible for repaying his or her issuing bank for the purchase and any accrued interest and fees associate with the card agreement.

[8]Network Fees/Assessments are the fees charged by the Networks (MasterCard and Visa) to facilitate the transactions through their systems. They charge basis points of the transaction in the range of around 0.05% with fluctuations of several basis points in either direction.

Acquirer/Processor fees are charged by the merchant processor/acquirer and are highly variable. They are normally in the 10s of basis points (ie .10%-.70%) as a percentage of a transaction.

In a hypothetical example Chase is the card issuer, Visa is the network, First Data is the processor/acquirer. Transaction value of $100 with a merchant discount of 2%. The merchant only has to pay that 2% (they will pay that to their processor, First Data in this case). That processor passes this information to Visa who then allocates the $2.00 the following ways.

Interchange (assume 1.65%) –> $1.65 to Chase (set by Visa based off of the credit card used in the transaction)

Network Fee (assume 0.05%) –> $0.05 to Visa

Processor/Acquirer Fee (assume 0.30% –> $0.30 to First Data

This is very high level. More parties often charge additional fees such as gateways and additional types of merchant processors making the dynamics of a transaction layered with many companies each taking a sliver. Additionally the interchange levels set by the networks are complex documents with discounts, fees and assessments applied to various merchant classes, geographies and card types

Retailers and consumers do not pay interchange. Interchange is the transfer rate exchanged between the retailer’s and cardholder’s financial institutions each time a Visa payment product is used. The retailer’s financial institution, or acquirer, generally pays interchange. Retailers make a payment to their financial institution for Visa card transactions, frequently referred to as a Merchant Discount Rate (MDR). This is a market-based fee set by each acquiring financial institution operating in a competitive marketplace—retailers can choose their financial institution in the same way cardholders can choose the financial institution that issues their Visa card.

Interchange plus pricing means that the provider charges a set fee — say 0.10 percent + $0.05 — over the interchange rate (the fees that go to the bank that issued the card used to purchase the goods and services) and the pass-through fees (the fees charged by the card companies).

The advantage of interchange plus pricing is that you have a processing rate that is determined up front. If an interchange rate is adjusted up or down, it automatically takes effect and will only affect the rate on a few of the cards. With no hidden costs and a statement you can actually understand, you will be receiving the most competitive pricing available and it’ll be easier for you to compare to the other processors.

With true interchange plus pricing, the actual costs are passed through to the merchant and all the costs of the processing are disclosed for the merchant to see, including interchange and the dues and assessment costs, the processor will then work with the merchant to establish the discount rate.

There are two main kinds of pricing merchant service providers use, interchange plus and tiered.

Interchange Plus

An interchange plus pricing model, is basically just a markup model. The merchant service provider adds up the interchange and card brand fees for a transaction and then adds their standard markup rate on top of that. The markup rate does not change based on card provider or type, making it a pretty transparent pricing model.

[11]‘Merchant Discount Rate’ is the fee, expressed as a percentage of the total transaction amount that a Merchant pays to its Acquirer or Service Provider for transacting a Credit Card…The Merchant Discount Rate shall include:

The Interchange Rate

Network set fees associated with the processing of a transaction

Network set fees associated with the acceptance of the network’s brand

The Acquirer set processing fees associated with the processing of a transaction; and

Any other services for which the Acquirer is paid via the mechanism of the per transaction merchant discount fee. Other than the fees listed in (a) through (d)

Retailers and consumers do not pay interchange. Retailers pay what is known as a Merchant Discount Rate (MDR) or Merchant Service Fee, which retailers can negotiate with their financial institution. The MDR usually includes the cost of transaction processing, terminal rental and customer service; interchange; as well as the acquirer’s profit margin, among other costs. Since interchange may be just one wholesale input into the Merchant Discount Rate, price caps on interchange would not necessarily lower a retailer’s cost for card processing.

[13] MasterCard publicly discloses all of its interchange rates on its website, and merchants are free to disclose these fees (or the merchant discount fees they pay) to their customers. Merchants may choose not to disclose these fees to consumers just as they choose not to disclose any other cost of doing business or how they price their merchandise.

Interchange is not a single amount. There are a number of interchange rates and they may vary by the type of retailer, cost of the sale, payment product type, processing technology the retailer uses and region or country. For example, transactions at fuel merchants and grocery stores each possess unique attributes that may require different interchange categories and processing strategies. Similarly, the type of payment product used and how that product is used affect the interchange rate and processing requirements. The different rates are used to encourage product and market development; data quality; and risk management programs and tools.

[14] With Interchange-plus pricing, you’ll get to see exactly how much money was paid to the card-issuing banks, how much went to the card associations, and how much went to Dharma.

With true interchange plus pricing, the actual costs are passed through to the merchant and all the costs of the processing are disclosed for the merchant to see, including interchange and the dues and assessment costs, the processor will then work with the merchant to establish the discount rate.

Tiered Pricing

Tiered pricing models are very different. They have vastly different rates for each kind provider and card used. Most of the time, there is no easy way to find out what those rates actually are, or how they compare to rates charged by other merchant service providers. This means it is much easier for the provider to rip you off.

We always recommend using a provider that will give you an interchange plus model of pricing.

[15] While interchange is not a direct cost to retailers, there is a cost to accept Visa cards, just as there is a cost to accept cash, cheques and other forms of payment. For example, it takes time to count and deposit cash, and cash may disappear as a result of errors or theft. Cheques can be delinquent or cause losses to retailers because of insufficient funds. The cost to accept electronic payments may be more transparent to retailers, however, because they are directly billed for the service by their acquirer.

Additionally, there are dues and assessment fees. These are passed onto the merchant. These are membership fees paid by financial institutions to VISA and MasterCard. These fees have no rules, category or criteria; they are just a set percentage of the amount of the sale and are the same for every transaction processed

[16] Myth: Interchange fees are a “hidden tax” on consumers.

Fact: In fact, interchange fees are not a hidden tax – they are neither hidden, nor a tax. Interchange is not paid by consumers. It is a fee paid between the merchant’s bank and the cardholder’s bank that serves to balance costs in the payments system. Interchange is a component of the merchant discount fee, which merchants pay for the extraordinary benefits they receive when they choose to accept payment cards. These include increased sales, fraud protection and faster payment, among other benefits.

Retailers do not pay interchange directly. They pay a Merchant Discount Rate that they can actively negotiate directly with their acquiring financial institution.

[17] The fees for any given transaction are broken down into two main categories: interchange costs along with dues and assessments and processor costs. Dues and assessments are paid to the networks which are Visa and MasterCard and are the same for everyone as are interchange costs. They are absolute and every processing company pays the same amount for interchange, dues and assessments.

[18] VISA and MasterCard publish these rates and requirements semi-annually. It is important to understand the fee amount is set by the sponsoring bank of the credit card and is the same for everyone, from Walmart right down to the smallest cornershop. The Interchange fees are updated every 6 months and any adjustments or increases only affect one or two interchange rates…additionally, there are dues and assessment fees. These are passed onto the merchant. These are membership fees paid by financial institutions to VISA and MasterCard. These fees have no rules, category or criteria; they are just a set percentage of the amount of the sale and are the same for every transaction processed…the most important thing to know is that the interchange fees and the dues and assessment costs are absolutely set and no one is paying more or less.

VISA and MasterCard publish these rates and requirements semi-annually. It is important to understand the fee amount is set by the sponsoring bank of the credit card and is the same for everyone, from Walmart right down to the smallest cornershop. The Interchange fees are updated every 6 months and any adjustments or increases only affect one or two interchange rates

The fees for any given transaction are broken down into two main categories: interchange costs along with dues and assessments and processor costs. Dues and assessments are paid to the networks which are Visa and MasterCard and are the same for everyone as are interchange costs. They are absolute and every processing company pays the same amount for interchange, dues and assessments. They cannot be changed or discounted for special situations or for any reason. So, whether you’re a fortune 500 processing company producing billions of dollars each year, or a hobby business with just a couple thousand dollars in volume, you pay the same fees.

[19] The fees for any given transaction are broken down into two main categories: interchange costs along with dues and assessments and processor costs. Dues and assessments are paid to the networks which are Visa and MasterCard and are the same for everyone as are interchange costs. They are absolute and every processing company pays the same amount for interchange, dues and assessments.

The most important thing to know is that the interchange fees and the dues and assessment costs are absolutely set and no one is paying more or less.

[20] What do merchants pay to accept Visa? Merchants pay fees to electronic payments service providers, referred to as an acquirer, or acquiring financial institutions for all the services the acquirer delivers. This fee usually includes the acquirer’s charges for acceptance of one or more payment brands and often includes account services, terminal purchase or rental and ongoing maintenance, security upgrades, fraud risk management, interchange, the use of data transmission lines, transaction slips and other card supplies, point-of-sale materials, as well as the acquirer’s profit margin. The aggregate of these fees are often called Merchant Discount Rates (MDR).

Merchant discount fees, which can include costs like processing transactions or terminal rental, are just one of many other costs a merchant incurs for running a business, such as electricity, rent or advertising costs.

[22]قال أبو جعفر (وأجر وزان الثمن على المشتري) وذلك لأن عليه تمييزه وإفرازه عن ماله وتسليمه إلى البيع ولا يعلم ذلك إلا بالوزن (وأجر كيال المبيع على البيّع) لهذه العلة بعينها

شرح مختصر الطحاوي للجصاص ت370ه (110/3) دار البشائر الإسلامية

“المادة ٢٨٨ المصاريف المتعلقة بالثمن تلزم المشتري مثلا أجرة عد النقود ووزنها وما أشبه ذلك تلزم المشتري وحده” لأن الوزن من التسليم وتسليم الثمن على المشتري فكذا ما يكون من تمامه (زيلعي) وكذا يجب عليه تسليم الجيد لأن حق البائع تعلق به فتكون أجرة نقد الثمن أي تعرف جيده من زيفه على المشتري كما في الكنز والتنوير وغيرها قال في البحر وما ذكره المصنف في نقد الثمن هو الصحيح كما في الخلاصة وهو ظاهر الرواية كما في الخانية وبه كان يفتي الصدر الشهيد وقال وبه يفتى إلا إذا قبض البائع الثمن ثم جاءه يرده بعيب الزيافة فإنه على البائع اهـ أي لأنه إذا قبضه دخل في ضمانه فإذا ادعى أنه خلاف حقه فالناقد إنما يميز ملكه ليستوفى بذلك حقا له فالأجرة عليه (حموي عن الجوهرة) وأطلق في أجرة الناقد فشمل ما إذا قال المشتري دراهمي منتقدة أولا وهو الصحيح خلافا لن فصل (بحر عن الخانية)

شرح المجلة للأتاسي d.1326 AH)) (219/2) مكتبة رشيدية

مسئلة البيت من الواقعات والنهاية قال في الواقعات أجرة الناقد على من تجب فهو على وجهين إما إذا قال المشتري من دراهم جياد أو قال غير منقود ففي الأول على البائع أن يجيء له بالناقد والأجر عليه وفي الثاني على المشتري والصحيح أنها على المشتري مطلقا وعليه فتوى الصدر الشهيد والخاصي وهو المفتى به في المذهب وقد فهم من البيت القول الآخر وقوله “والشرط ليس يغير” أراد به اشتراط المشتري أن الدراهم جياد وأن هذا لا يغير فلا يجعل النقد على البائع كما هو القول المرجوع وذكر في النهاية أنه روي عن محمد أنه جعل أجرة الناقد على من عليه الدين إلا أن يقبض رب الدين دينه ثم يدعي أنه من غير نقد فيكون الأجر على رب الدين وفي واقعات الخاصي عن القدوري أنها على المشتري إلا إذا قبض البائع الثمن ثم جاء يرده بعيب الزيافة والله أعلم

شرح منظومة ابن وهبان لإبن الشحنة (d.921 AH) (282/1) الوقف المدني

[23] المادة ٢٨٩ “المصاريف المتعلقة بتسليم البائع وحده مثلا أجرة الكيال للمكيلات والوزن للموزونات المبيعة تلزم البائع وحده”

وكذا أجرة العداد والفراع إذا بيعت بشرط العد والذرع اهـ (مسكين) لأن التسليم عليه وهذا من تمامه ولو اشترى حنطة في سنبلها فعلى البائع تخليصها بالدرس والتدربة ودفعها للمشتري هو المختار والتبن للبائع – إلا إذا بيعت بما هي فيه يعني إذا باع الحنطة بالتبن فإنه لا يلزم البائع تخليصه (رد المحتار) أي والمشترى يكون للمشتري كما هو ظاهر ولو اشترى ثيابا في جراب ففتح الجراب على البائع وإخراج الثياب على المشتري إلا إذا كان العرف بخلافه كما لو اشترى ماء في قربة فإن صبه يكون على البائع (أبو السعود) لكن قال الحموي إخراج الثياب من الجراب من تمام التسليم فينبغي أن يكون على البائع…

شرح المجلة للأتاسي d.1326 AH)) (220/2) مكتبة رشيدية

[24]Interchange is a component of the merchant discount fee, which merchants pay for the extraordinary benefits they receive when they choose to accept payment cards. These include increased sales, fraud protection and faster payment, among other benefits.

NOTE: Even in Tiered Pricing, the Interchange of that transaction could possibly be calculated, but it would be more difficult

Unsurprisingly, most credit card schemes, which opposed the payments system reforms, are also strongly opposed to merchant surcharging. These fees directly impact on the likelihood that consumers will use their cards. Visa thinks merchants should include the acceptance costs in their price, just as a shop does with other expenses such as providing a car park or paying staff more on a Sunday, (even though not all customers drive, or shop on a Sunday). “One of the core tenets of the consumer experience is that the price of an item as advertised or on the price tag should be the actual price paid at the checkout,” argues General Manager Chris Clark. “This fundamental consumer protection has been recognised by governing bodies around the world. If more merchants impose surcharges, it will unfairly penalise consumers at a time when they are already facing the challenges of a difficult economy and increased cost of living expenses.” MasterCard’s opposition to surcharges is also fundamental – “our core issue is that surcharging passes the cost of accepting payment onto consumers. And that’s absolutely not fair,” says David Masters, Vice President, Strategy & Corporate Affairs. MasterCard argues that accepting card payments is a normal cost of doing business and shouldn’t be separately charged. “Merchants get a lot of benefits from cards that they don’t get from cash or cheques. Obviously, instant payment and protection from credit losses and fraud. And, when they accept a payment by card (as opposed to cash) the money goes straight into their account without having to protect and transport it. And the big difference – the existence of credit cards provides merchants with sales they wouldn’t get if people could only spend the cash they could carry in their wallet. Before credit cards as we know them today, the extension of credit was something retailers did themselves – that risk (fraud losses) is now carried by banks.” American Express also told us that it believes the costs of card payments are, like all other costs, already built into the cost of goods sold. And the card industry regularly points out that its main competitor – cash – has associated costs for retailers that are often ignored. 1 A Qantas spokesperson says, “Qantas strongly rejects any suggestion, including by CHOICE, that its card payment fees are somehow ‘shonky’ or that Qantas is gaining a windfall from them …”. See further comments, page 18. CHOICE REPORT: Credit card surcharging in Australia Prepared on behalf of NSW Fair Trading CHOICE REPORT: Credit card surcharging in Australia Prepared on behalf of NSW Fair Trading 9 We only found one credit card scheme – Diners Club – that hasn’t taken a public stand against surcharging. Perhaps one factor is because, as the smallest and least-accepted card scheme, it has less bargaining power with retailers than the others. “We have never sought to discourage our merchants from asking for whatever payment method they prefer, so the regulation of surcharging was not an issue for us,” it said in 2006 evidence to a House of Representatives hearing. “We regard surcharging as an issue between the retailer and the customer, not between the retailer and us. If the retailer believes that it is positive for their relationship with their customer to negate and refuse their payment choice, then that is what the retailer should do. Retailers in more competitive situations have chosen not to do that. Our observation is that retailers who feel they are subject to less competitive pressure have tended to surcharge

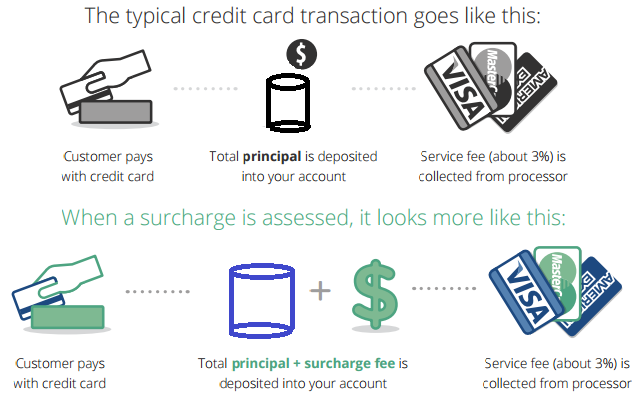

Payment Surcharge A payment surcharge is an additional fee payable by the buyer (client, customer; hereinafter “customer”) to the seller or seller’s representative (trader, firm, merchant; hereinafter “merchant”) for using a particular form of payment, such as a debit card. A payment surcharge can take the form of a fixed fee per transaction; a percentage of the transaction value; or a fee per item purchased. For example, a payment surcharge on a single purchase of ten items costing £1 each (£10 in total) may appear as:

10 £10 transaction value + 1% surcharge = £10.10

£10 transaction value + £1 surcharge per transaction = £11

£10 transaction value + £1 surcharge per item = £20

Fees payable by a merchant (such as card processing fees) to the payment service provider (or ‘acquirer’) for on-line payments are not payment surcharges, because they are levied by the acquirer, not the merchant, IN RETURN FOR PAYMENT SERVICES PROVIDED TO THE MERCHANT.

Estimated total value of card payment surcharges in the UK in 2010 (millions)

The term, “credit card surcharging,” is still not well known. Maybe it’s because the practice is so new and very few merchants are doing it. Maybe it’s because the word “surcharge” has a negative connotation, and is often dismissed by many merchants as ANTI-CONSUMER.

[26]RETAILERS LARGELY DO NOT APPLY PAYMENT SURCHARGES AT THE POINT OF SALE. The EDC survey2 indicated that almost no retailer applied a surcharge to over-the-counter cardholder-present transaction (i.e., surcharging in store was very rare). There are two main reasons why retailers do not tend to surcharge over-the-counter transactions: (i) competition within the retail sector puts any retailer that imposes a payment surcharge at a competitive disadvantage; and (ii), it is difficult for retailers to distinguish card types at the point of sale in store. According to the British Retail Consortium, there are currently over 270 different card types in the UK. Complex hardware, software and staff training would be required to implement an accurate surcharging mechanism and process at the point of sale.

SMALL BUSINESSES LARGELY DO NOT APPLY PAYMENT SURCHARGES, for the same reasons as larger retailers. However, some small businesses like corner shops, pubs and off licenses apply a payment card surcharge, particularly for low value transactions (typically under £10) or do not accept card payments for less than this value. Options 2 to 4 assume that SMEs will be exempted from a surcharging ban until June 2014 as part of the Government’s moratorium on new regulation for SMEs4 . From June 2014 the Government will be required to give full effect to the Consumer Rights Directive and will be obliged to apply the ban to all businesses operating within the scope of the Directive. Options 1 and 2 will enable small businesses to continue to recover the reasonable direct costs they incur in accepting card payments.

SERVICE SECTOR: PAYMENT SURCHARGES ARE COMMON IN THE AIRLINE SECTOR, and less frequent in other sectors, notably rail, ferries, taxis, event tickets, cinemas, car dealerships, holidays, hotels and parking. As in the retail sector, payment surcharges seem to apply most commonly to on-line and telephone transactions (card-not-present transactions), rather than face to face. Payment cards are often the only payment method offered by merchants for on-line transactions in the UK.

Business to business: PAYMENT SURCHARGES ARE NOT COMMON PRACTICE.

Third sector: PAYMENT SURCHARGES ARE NOT COMMON PRACTICE.

Central and Local Government: Some Government agencies and local councils have begun to impose credit card surcharges to recover the costs they incur on accepting credit card payments, for example for paying council tax, business rates or planning application fees, or buying a tax disc from the DVLA, or making some tax payments to HMRC.

[27]Q. Does the ability to surcharge apply to merchants globally? No. The settlement agreement impacts Visa’s rules related to the surcharging of credit card purchases made in the U.S. and U.S. territories only. Surcharging remains prohibited outside the U.S. unless there is a local law or variance that requires merchants be permitted to engage in the practice.

Since January 27, 2013, merchants in the United States and U.S. Territories have been permitted to impose a surcharge on consumers when they use a credit card.

Retailers must limit the amount of the surcharge to the merchant discount rate for the credit card transaction surcharged, or 4%, whichever is lower.

Charge a fee to use your credit card? It’s legal for merchants to do that, unless barred by state law. Ten states already ban such surcharges — California, Colorado, Connecticut, Florida, Kansas, Maine, Massachusetts, New York, Oklahoma, and Texas — and more may join the list.

[30]“Surcharge” means any fee charged by the Merchant for the use of a card. As set forth in this rule 5.11.2 of chapter 10, a merchant located in American Samoa, Goam, or the Northern Mariana Islands may only require a MasterCard Credit Cardholder to pay a surcharge by choosing to apply either of the following surcharge methods:

Brand-level surcharge – The application of the same surcharge to all MasterCard Credit Card Transactions regardless of the Issuer

Product-level Surcharge – The application of the same surcharge to all MasterCard Credit Card Transactions of the same product type regardless of the Issuer

[31]فإن العرف العام يصلح مخصصا كما مر عن التحرير ويترك به القياس كما صرحوا به في مسئلة الإستصناع ودخول الحمام والشرب من السقا

نشر العرف لإبن عابدين (d.1252 AH) (85) مركز البحوث الإسلامية مردان

الثابت بالعرف قاض على القياس ولذا جاز بيع النعل مع شرط التشريك بالعرف والقياس أن لا يجوز لأن فيه شرطا لا يقتضيه العقد وفيه منفعة لأحد العاقدين لا يقال نهى النبي صلى الله عليه وسلم عن بيع وشرط وهو بإطلاقة يقتضي عدم جوازه العرف ليس بقاض عليه! لأنه معلول بوقوع النزاع المخرج للعقد عن المقصود به وهو قطع المنازعة والعرف ينفي النزاع فكان موافقا لمعنى الحديث فلم يبق من الموانع إلا القياس على ما لا عرف فيه بجامع كونه شرطا والعرف قاض عليه

(أما معناها: فهي مكونة من اصطلاحين رئيسين الأول منهما مقدم على الآخر وهما العرف والقياس وبالتأمل في شرح المؤلف للقاعدة والسياق التي وردت فيه في الكتب السابقة يتبين أن مرادهم بالعرف العرف العملي العام الذي قد يكون بمثابة الإجماع العملي بل سبق أن صرح المؤلف بهذا عند شرحه لقاعدة “إجماع المسلمين حجة يخص بها الأثر ويترك القياس والنظر” حيث قال في نهاية شرحها “…وترك القياس بإجماع المسلمين” وهذا مراد القوم مما قالوا “الثابت بالعرف قاض على القياس” كما صرح بذلك صاحب العناية وصاحب مجمع الأنهر ود. أحمد أبو سنة – وقد سبق نقل تصريحاتهم عند توثيق القاعدة -. ويلحظ من السياق أيضا أن مرادهم بالقياس القياس الذي بمعنى القاعدة العامة وليس القياس المشهور عند الأصوليين وقد نبة على ذلك أ.د. أحمد أبو سنة في كتابه: العرف والعادة)

ترتيب اللآلي لناظر زاده (كان حيا سنة 1061 AH) (579) مكتبة الرشد

(المادة ١٨٨ البيع بشرط متعارف يعني الشرط المرعي في عرف البلدة صحيح والشرط معتبر)

أي وإن كان لا يقتضيه العقد ولا يلائمه وأفادت هذه الجملة أنه يعتبر العرف الخاص الحادث قال في رد المحتار: ومقتضى هذا أنه لو حدث عرف في شرط غير الشرط في النعل والثوب والقبقاب أن يكون معتبرا إذا لم يؤد إلى المنازعة وانظر ما حررناه في رسالتنا المسماة نشر العرف في بناء بعض الأحكام على العرف وحاصل ما حققه في تلك الرسالة أن العرف الخاص معتبر وإن خالف المنصوص عليه في كتب المذهب ما لم يخالف النص الشرعي يعني الكتاب والسنة والإجماع وإن العرف الخاص يشمل القديم والحادث وإن حكم العرف يثبت على أهله خاصا أو عاما فالعرف العام في سائر البلاد يثبت حكمه على أهل سائر البلاد والعرف الخاص في بلدة واحدة يثبت حكمه على أهل تلك البلدة وأنه إنما يعتبر العرف سواء كان خاصا أو عاما إذا كان شائعا بين أهله مستفيضا لديهم يعرفه جميعهم وساق الأدلة على جميع ذلك من نصوص المذهب متونا وشروحا وفتاوى شكر الله سعيه وجزاه خيرا

شرح المجلة للأتاسي (d.1326 AH) (64/2) مكتبة رشيدية

ثم اختلفت عبارات الفقهاء الحنفية في تعليل فساد البيع بالشرط فقد مر عن البدائع أن فساد البيع في مثل هذه الشروط لتضمنها الربا وذلك بزيادة منفعة مشروطة في العقد لا يقابلها عوض وقال ابن عابدين رحمه الله تعالى إنه معلل بإفضاءه إلى النزاع فقال معللا لجواز الشرط المعروف: “لأن الحديث معلول بوقوع النزاع المخرج للعقد عن المقصود به وهو قطع المنازعة والعرف ينفي النزاع فكان موافقا لمعنى الحديث” والظاهر أن تعليل ابن عابدين رحمه الله تعالى هو الراجح وذلك لأمرين الأمر الأول: أن الفقهاء الحنفية أجازوا الشروط التي جرى التعامل بها بحكم العرف ولو كان الفساد معلولا بكون العقد يتضمن الربا لما جاز الشرط بحال حتى لو كان متعارفا لأن الربا لا يحل بالعرف والتعامل.

والأمر الثاني: أن تعليله بأنه زيادة من غير عوض ويلزم منه الربا غير واضح لأنه إذا اشترط المشتري منفعة فإن تلك المنفعة صارت جزء من المبيع وصار جزء من الثمن مقابلا لها وإن اشترط البائع منفعة صارت تلك المنفعة جزء من الثمن وصار جزء من المبيع مقابلا لها فليس هناك زيادة بغير عوض نعم! يلزم منه صفقة في صفقة على أن جزء المبيع المقابل للمنفعة في الصورة الأولى وجزء الثمن المقابل للمنفعة في الصورة الثانية غير معلوم فجاء الفساد من هذه الجهة وهو الذي عبر عنه المالكية بأنه يخل بالثمن كما أسلفنا في مذهبهم فتبين أن العلة هي الجهالة المفضية إلى النزاع وليس أنه زيادة من غير عوض أما إذا كان الشرط متعارفا فالعرف يقضي على أنه ليس صفقة في صفقة لأن مجموع ما عقد عليه الأمر أصبح بحكم العرف كأنه شيء واحد فصار كما باع شاتين بصفقة واحدة وإن العرف يقضي على الجهالة أيضا لكون التجار يعرفون فرق السعر بين البيع المشروط فيه المنفعة وبين غير المشروط فيه فلا يقع النزاع عند الإخلال بالشرط فإن اشترط مشترى النعل أن يحذوه البائع فإن الفرق بين قيمة المحذو وغير المحذو معروف بين التجار ثم إن الحنفية ذكروا صورا أخرى للشرط المتعارف غير شرط حذو النعل فقال ابن الهمام رحمه الله تعالى “ومثله في ديارنا شراء القبقاب على هذا الوجه أي على أن يسمر له سيرا ومن أنواعه شراء الصوف المنسوج على أن يجعله البائع قلنسوة وبشرط أن يبطن لها البائع بطانة من عنده” وجاء في البزازية “اشترى ثوبا أو خفا خلقا على أن يرقعه البائع ويسلمه صح” وقال ابن عابدين رحمه الله تعالى “وتدل عبارة البزازية والخانية وكذا مسألة القبقاب على اعتبار العرف الحادث ومقتضى هذا أنه لو حدث عرف في شرط غير الشرط في النعل والثوب والقبقاب أن يكون معتبرا إذا لم يؤد إلى المنازعة”

فقه البيوع لمفتي تقي عثماني (500/1) مكتبة معارف القرآن

[32]Merchant registration with MasterCard and acquirer

A merchant’s ability to apply a surcharge is conditioned on the merchant’s satisfaction of certain disclosure requirements. These disclosure requirements include advance notice to both MasterCard and the merchant’s acquirer of the merchant’s intention to impose a surcharge no less than thirty days before the merchant implements a surcharge. A merchant can satisfy its disclosure obligation to MasterCard by clicking here and providing the following information:

Merchant Name

Merchant Contact Information (address, phone and email)

Number of Locations Surcharging

Type of Channel (face-to-face, eCommerce, mail order or phone order)

Type of Surcharge (brand or product)

Merchants should contact their acquirers with regard to the acquirer notification requirements.

Type of permissible surcharges

Merchants are permitted to apply either a brand-level surcharge or a product-level surcharge to MasterCard credit cards. A brand level surcharge is one where the merchant charges the same percentage on all MasterCard credit cards. A product level surcharge is one where the merchant imposes a surcharge on a particular MasterCard credit product. In both circumstances, the level of the surcharge is subject to a cap.

Cap on the level of the surcharge

The level of the fee that a merchant may charge a cardholder is capped in relation to the merchant’s cost for MasterCard credit acceptance. For merchants who choose to impose a brand level surcharge, a merchant may only surcharge a MasterCard cardholder at the lesser of the merchant’s average effective merchant discount rate that the merchant pays its acquirer for MasterCard credit acceptance or the Maximum Surcharge Cap, which can be found below. For merchants that impose a product level surcharge, the surcharge must not be more than the merchant’s cost to accept the particular MasterCard credit product, minus the Durbin Amendment’s cap on debit interchange fees.

Merchant disclosure to consumer

A merchant must provide clear disclosure to the merchant’s customers of the merchant’s surcharging practices at the point of interaction which shall include the amount of the surcharge and the dollar amount of the surcharge on the transaction receipt provided by the merchant to its customers. Merchants should refer to the specific rule for additional consumer disclosure obligations.

Nothing in the MasterCard rules affects any obligation of a merchant to comply with applicable state or federal laws, including but not limited to state laws that may prohibit or restrict surcharging of credit transactions, and federal and state laws regarding deceptive or misleading disclosures.

Other requirements should the merchant accept competing credit networks

For merchants that accept other brands of credit payment networks, such as American Express, Discover or PayPal, there are other requirements around the circumstances in which such a merchant could surcharge MasterCard cards that depend on the costs of those brands to the merchant and those brands’ surcharging restrictions. A merchant should refer to the specific rules and/or contact their acquirer for greater detail concerning those requirements.

Myth: Merchants have no choice but to pay a set interchange fee.

Fact: If a retailer is dissatisfied with the merchant discount rate it negotiated with its bank for MasterCard acceptance, that retailer has several options: it can provide discounts to those who pay with cash or check, negotiate a different merchant discount rate with its bank or switch to a bank that offers more competitive rates, or choose not to accept MasterCard cards. There is significant competition for merchant acceptance among financial institutions and payment card providers. Merchants, of course, are free to choose which payment options they accept and can choose to encourage their customers to use a particular payment choice.

Retailers have options for lowering their costs if they genuinely believe their electronic payment acceptance costs are too high. They can reduce payment card volume by providing discounts to those who pay with cash, or choose to accept only cash or cheques. Or, retailers can shop around among competing acquiring financial institutions for the best prices.

[34]A payment card surcharge, also known as a checkout fee, is an additional fee that a merchant adds to a consumer’s bill when he or she uses a card for payment.

Do not set minimums and maximums and do not surcharge you should not…impose a surcharge as a condition for accepting payment by Visa cards. Doing so can damage your relationship with your own customers and you may also lose new sales opportunities. Visa’s research has shown that many cardholders won’t do business with merchants who require minimum purchases on their Visa cards.

Merchants are charged several fees for accepting credit cards. The merchant is usually charged a commission of around 1 to 4 percent of the value of each transaction paid for by credit card. The merchant may also pay a variable charge, called a merchant discount rate, for each transaction. In some instances of very low-value transactions, use of credit cards will significantly reduce the profit margin or cause the merchant to lose money on the transaction. Merchants with very low average transaction prices or very high average transaction prices are more averse to accepting credit cards. In some cases merchants may charge users a “credit card supplement” (or surcharge), either a fixed amount or a percentage, for payment by credit card.This practice is prohibited by most credit card contracts in the United States, and is actually illegal in 10 states although the contracts allow the merchants to give discounts for cash payment.

[36]Pursuant to a settlement of the U.S. merchant class litigation, MasterCard will modify certain rules and business practices to permit U.S. merchants to apply an extra checkout fee, also known as a surcharge, to customers who pay with MasterCard-branded credit cards. The rule change permitting such surcharging will go into effect on January 27, 2013. These fees are not allowed on Debit MasterCard or MasterCard prepaid cards.

The following nine states currently have laws prohibiting credit card surcharges: California, Colorado, Connecticut, Florida, Kansas, Maine, Massachusetts, Oklahoma, Texas. New York’s “no surcharge” statute was just declared unconstitutional by a federal judge and is no longer enforceable. The other states’ statutes also face constitutional challenges.

Q. Can I assess a surcharge on both credit and debit card purchases? No. The ability to surcharge only applies to credit card purchases, and only under certain conditions.U.S. merchants cannot surcharge debit card or prepaid card purchases.

[37]Thirdly, even if the government is not a pure Islamic government, every citizen enters into an express or a tacit agreement with it to the effect that he will abide by its laws in so far as they do not compel him to do anything which is not permissible in Shari’ah. Therefore, if the law requires a citizen to refrain from an act which was otherwise permissible (not mandatory) in Shari’ah, he must refrain from it.

بدائع الصنائع للكاساني ت587ه (532/6) دار الكتب العلمية

سوال مال تجارت پر منافع لینے کی کوئی تعداد اگر ہو تو ضرور تحریر فرمائیں-

جواب: شرعا کوئی تعداد مقرر نہیں مگر زیادہ نفع لینا مروت کے خلاف ہے

فتاوی محمودیۃ (48/16) دار الافتاء جامعیہ فاروقیہ